Why BFSI Automation Is Shifting From Workflows to AI Agents

05 Feb 2026

Table of Contents

Banking is not losing to fintech because it lacks features. It is losing time in execution. A customer uploads KYC docs, but the verification queue is backlogged. A fraud alert fires, but outreach happens through a tool that is not tied to the customer record. A complaint arrives, but it bounces across teams before anyone can answer a simple question: “What happened, and what do we do next?”

That gap between decision and action is where trust breaks. AI agents close it with governed action, not more dashboards. They can interpret data and trigger approved steps like updating records, escalating cases, or sending alerts within compliance guardrails.

This is also why the Salesforce Spring ’26 financial services updates matter. They are not random feature drops. They are signals that the platform is preparing for agent-led operations, where clean relationship structures, compliant servicing, and scalable voice experiences become prerequisites, not nice-to-have.

Table of Contents

What AI Agents Really Mean for Modern Banking

An AI agent is a software “doer,” not just a software “talker.” A simple way to define it for BFSI leaders:

AI agents are autonomous software programs that can interpret data, decide what to do next, and take action toward a goal, within guardrails you control.

That definition matters because a lot of tools get mislabeled as agents.

What AI Agents are Not

Chatbots: They can talk, but they often cannot execute. They answer, then hand off.

RPA (Robotic Process Automation): It can execute, but without judgement. It follows rigid steps and fails when exceptions show up.

Workflows: They are great until reality gets messy. And banking is always messy.

Why Banking Is the Perfect Agent Environment (and the Most Unforgiving)

Banking has the exact workload shape that agents handle well:

- High volume

- Exception heavy

- Time sensitive

- Regulated

- Distributed across systems and channels

The problem is not effort. It is context.

In many service teams, 26% of reps say they often lack context about a customer’s situation, and 80% say better access to other departments’ data would improve their work. When context is missing, even simple cases become slow. The agent has to hunt for details, repeat questions, and manually stitch together the story.

It also explains why capacity feels tight even when headcount does not change. Agents spend only 39% of their time actually servicing customers, while the rest goes into internal meetings, admin work, and manually logging notes. In a regulated environment, those “non-service” minutes are not optional, but they are a clear signal that the operating model is overloaded.

Where Agents Win

Agents win when the work needs orchestration across systems and continuity across channels.

Customers do not experience “core banking,” “CRM,” “KYC vendor,” and “collections.” They experience one bank. Agents help you operate like one bank by carrying context forward, pulling the right data at the right time, and executing the next step without forcing humans to do the stitching.

Where Agents Fail

Agents fail when the foundation is weak:

- Relationship data is inconsistent

- Governance is unclear

- Actions are not permissioned by scenario

- Audit trails are missing or scattered

In other words, agent-led banking breaks down when trust and control are not built into the process. That is why Spring ’26 leans into structure and governance capabilities like Flexible Hierarchies and Complaints Management. Agent-led execution depends on clean relationship context, clear ownership, and controlled escalation paths.

Want to Know How Salesforce Spring 26 Can Help Your Teams?

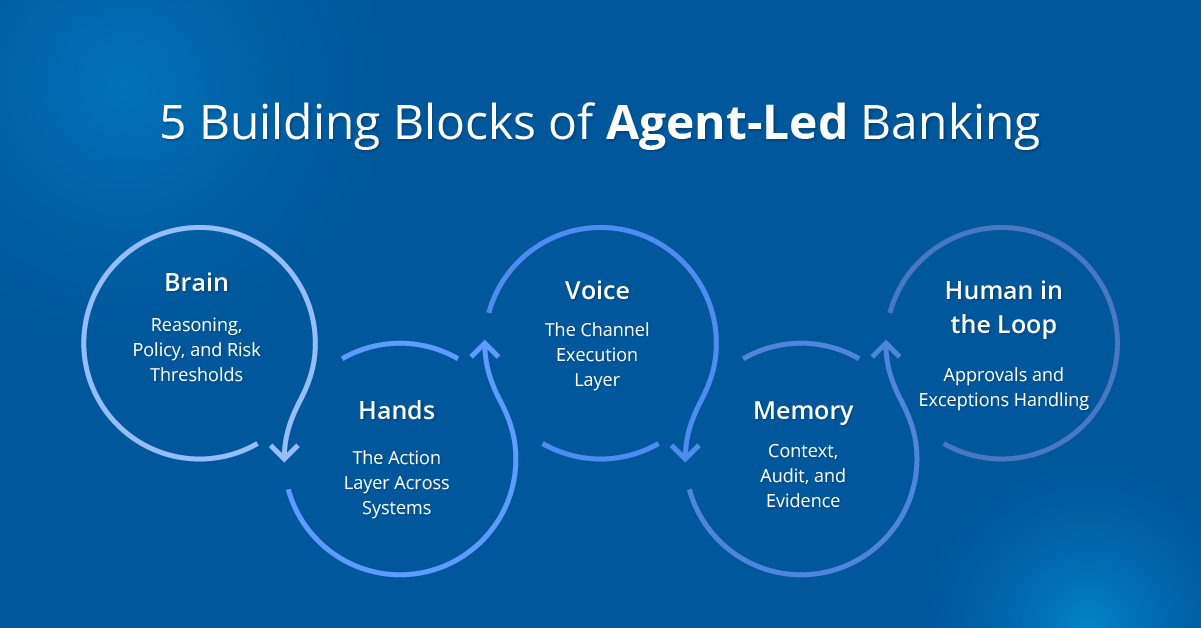

The 5 Layers of an Agent-ready Banking Stack

Think of agentic AI in banking as a stack, not a single feature. Many teams focus on building the “brain” first, then wonder why the program struggles in production. In real AI agents in financial services deployments, success depends on whether the agent can make safe decisions, take controlled actions, communicate through governed channels, and leave a clean audit trail.

1. Brain: Reasoning, Policy, and Risk Thresholds

This is the decision layer. It figures out what the customer is trying to do, what the best next step is, and whether the agent can do it automatically. In AI agents in banking, this usually looks like intent detection, next best action logic, and a risk score that decides when to proceed, when to ask a clarifying question, and when to escalate. The most important part is the “allowed actions” matrix. Agents do not need unlimited power. They need clearly bounded power based on scenario, risk level, and confidence.

2. Hands: The Action Layer Across Systems

This is the execution layer. An agent becomes valuable only when it can take controlled action and write back to the system of record. For AI agents for BFSI, that means connecting to the tools where work actually happens, like Salesforce Financial Services Cloud records, case creation, routing and queues, onboarding and KYC handoffs, fraud ticketing, and knowledge retrieval. The point is simple: the agent should not just recommend. It should complete the next step safely and document it.

3. Voice: The Channel Execution Layer

This is where many automation programs quietly lose value. Even if an agent decides the right next step, execution fails when customer communication happens outside the governed system. That is when context gets lost, consent handling becomes inconsistent, notes get copied manually, and audit trails become messy. A strong channel layer keeps conversations connected to records across SMS, WhatsApp, email, and calls, while enforcing opt outs and policy rules. In many Salesforce environments, this is where tools like 360 SMS and 360 CTI fit naturally as execution rails, because they help keep outreach and escalations tied to the same case and compliance controls. The agent decides, and the channel layer helps it act without breaking governance.

4. Memory: Context, Audit, and Evidence

In banking, memory is not chat history. It is evidence. A safe agent needs interaction logs attached to the customer record, a decision trail that shows why it acted or escalated, and outcome tracking so teams can monitor performance and improve over time. This is how you defend decisions, support compliance, and build confidence in scaling AI agents in financial services beyond pilots.

5. Human in the Loop: Approvals and Exceptions Handling

Agent-led banking does not remove humans. It protects human time for the moments that need judgment. High risk actions should require approvals, and low confidence situations should route to a supervisor queue. When escalation happens, the handoff should include a clean summary, transcript, and recommended next step so the human does not restart the investigation from scratch. This layer is what makes agentic AI in banking feel trustworthy, especially in fraud, disputes, hardship cases, and KYC exceptions.

Where AI Agents Fit Best in Banking: 3 High Impact Plays

The smartest banks are not trying to automate everything at once. They are picking a few customer journeys where context is fragmented and execution is slow, then using agents to orchestrate actions across systems and channels with clear guardrails. Start with these three high-impact plays.

Play A: Onboarding and KYC Completion That Reduces Drop-Offs

This is where “trust speed” becomes measurable. What happens today:

- Missing documents stall onboarding

- Applicants abandon mid flow

- Teams follow up manually across channels

- Status updates live in portals, not in the relationship view

What an agent changes:

- Detects missing documents and nudges the customer

- Verifies completeness against policy rules

- Updates onboarding status in Salesforce

- Routes exceptions to the right queue with context

This is not about “sending reminders.” It is about closing the loop between customer action and bank action, without waiting for humans to stitch context together.

Play B: Fraud Triage and Customer Verification That Moves at Fraud Speed

Fraud is the ultimate agent test because it mixes urgency, risk, and compliance.

Salesforce frames fraud as a core AI agent use case and points to rising consumer interest in AI that prevents and detects fraud.

What an agent can do safely:

- Monitor signals and patterns

- Trigger verified outreach for confirmation

- Escalate based on response or non-response

- Log every step back to the customer record

Google Cloud’s 2025 research also shows fraud management and detection is among the most adopted use cases for AI agents in financial services, alongside risk management.

The outcome is not just faster containment. It is fewer false positives that annoy good customers, because context and history are part of the decision.

Play C: Smart Servicing That Deflects Volume Without Breaking Trust

If your service cost reduction depends on pushing customers into self-service that feels like a maze, you are not reducing cost. You are shifting pain. An agent is different because it can resolve, not just route.

Common servicing actions agents can handle within guardrails:

- Case status checks and proactive updates

- Card replacement workflows

- Address updates with verification

- Dispute intake and evidence capture

- Collections questions with clear policy grounded answers

And when it cannot resolve, it escalates with a full summary so the human does not restart the story.

This is where the “Voice” layer becomes powerful, because servicing is not only digital chat. It is SMS nudges, WhatsApp updates, and voice calls when the situation is sensitive.

What Salesforce Spring ’26 Signals for Agent-led Financial Services

Spring ’26 makes the direction clear. Salesforce is shaping Financial Services Cloud for an agent-ready operating model, where AI can act with control, not just assist with answers. Here are the signals, mapped to the agent stack:

- Voice is becoming a first-class agent channel. Agentforce Voice for Financial Services strengthens the Voice layer for everyday servicing and collections with customer identification and natural conversations.

- Complaints are being treated as a governed workflow. Complaints management strengthens the brain and human oversight layers with consistent capture, routing, escalation, and guidance.

- Relationship context is becoming infrastructure. Flexible hierarchies strengthens memory and decision context by mapping households, ownership structures, and complex client relationships.

- Origination ecosystems are getting streamlined. Financial Intermediary Center strengthens the Hands layer through faster onboarding, simplified registration, and cleaner commission operations.

- Operational exceptions are being reduced upstream. Insurance Billing strengthens Hands and operational memory with flexible billing and automated commission tracking and reconciliation.

What 360 SMS and 360 CTI Enable in an Agent-led Operating Model

AI agents can decide the right next step, but execution breaks when customer communication happens outside Salesforce. Context gets lost, follow-ups become manual, and audit trails get fragmented. A Salesforce-native messaging and voice layer keeps the full journey record tied and executable.

- 360 SMS: Record-tied Messaging That Turns Agent Decisions into Customer Actions

360 SMS lets agents run two-way customer journeys over SMS and WhatsApp directly inside Salesforce. Messages and replies stay connected to the right Lead, Contact, or Case, and responses can auto-update Salesforce. This makes it practical to run onboarding nudges, verification prompts, surveys, and follow-ups at scale. It also supports AI language translation, helping teams engage customers in their preferred language while keeping the workflow consistent.

Ready to Fast-Track Your Banking Operations With 360 SMS?

360 CTI: Salesforce-native Voice for High-trust Moments

360 CTI brings calling into Salesforce through Open CTI with auto-logged interactions. It adds real-time call transcription and AI coaching to improve call quality and first-call resolution. For scale, it supports IVR, automatic call distribution, and power dialer workflows. When needed, an AI voice bot can handle common inbound and outbound conversations like qualification, queries, and booking.

What This Looks Like in Core Banking Plays

- Onboarding and KYC: 360 SMS sends document requests and reminders, captures replies, and updates status in Salesforce. If the customer is stuck or unresponsive, 360 CTI escalates to a call with the same record context.

- Fraud verification: 360 SMS runs time-bound verification flows with follow-ups. If the signal is ambiguous or there is no response, 360 CTI moves it to voice with transcription and logging for evidence.

- Servicing and collections: 360 SMS handles proactive updates and reminders. 360 CTI supports sensitive conversations through routed calls, IVR, and coached agent responses.

- Simple model: AI agents decide the best next action. 360 SMS and 360 CTI execute it through record-tied messaging and calling inside Salesforce.

Want to Know More About How 360 CTI Can Streamline Your Banking Processes?

Conclusion

Workflow automation helped banks digitize processes. AI agents will help banks operationalize trust at speed. That is the difference. Agents do not replace governance. They force you to make governance executable. They do not remove humans. They protect humans from the churn of repetitive work and reserve human attention for the moments that actually matter. Spring ’26 makes the direction clearer than ever: relationship structure, complaint governance, and voice scale are becoming core building blocks for agent-led financial services.

If you want a practical next step, start here: map your top three journeys across onboarding, fraud, and servicing, then identify where the “Voice layer” breaks today because the conversation is outside the customer record. That is usually where the fastest, safest wins show up first.

Want Agent-led Banking Inside Salesforce?

Our experts would help you map onboarding, fraud, or servicing and turn it into an executable flow. Just drop us a line at contact@360degreecloud.com, and we’ll take it from there!

Categories

Solve It with Salesforce. We’ll Show You How.

AI. Apps. Experts. Everything you need to win with Salesforce under one roof.Frequently Asked Questions

What should a bank automate first when adopting AI agents?

Start with one high-volume journey where policies are clear and outcomes are measurable, like KYC completion, fraud verification, or case status servicing. The best first choice is the one with the most manual follow-ups and the simplest approval boundaries.

What data do AI agents need to work reliably in banking?

At minimum, agents need trusted customer identity, consent status, current case or application stage, and interaction history. For complex relationships, they also need household or ownership context so they do not make decisions on incomplete relationship data.

How do AI agents reduce cost-to-serve without hurting customer experience?

They reduce repeat contacts by proactively updating customers, resolving routine requests end-to-end, and escalating only when needed with a full summary. The goal is not deflection at any cost, it is faster resolution with fewer handoffs.

How do banks measure success for agent-led onboarding, fraud, and servicing?

Track metrics tied to execution speed and trust: onboarding completion rate and time to KYC, fraud time to verify and false positive rate, service containment rate, average handling time, and complaint time to resolution.

How does Salesforce Spring ’26 help banks scale agent-led operations?

Spring ’26 strengthens the foundations agents depend on: voice automation for servicing and collections, governed complaint handling, clearer relationship hierarchies, streamlined intermediary origination, and more automated billing and reconciliation. These reduce exceptions and improve control as autonomy scales.

About the author

Editorial TeamThe Editorial Team at 360 Degree Cloud brings together seasoned marketers, Salesforce specialists, and technology writers who are passionate about simplifying complex ideas into meaningful insights. With deep expertise in Salesforce solutions, B2B SaaS, and digital transformation, the team curates thought leadership content, industry trends, and practical guides that help businesses navigate growth with clarity and confidence. Every piece we publish reflects our commitment to delivering value, fostering innovation, and connecting readers with the evolving Salesforce ecosystem.

Recent Blogs

Salesforce Services

Salesforce Services

Your Current Contact Center is Obsolete- Salesforce Proves It

We’ve all been there: explaining a complex issue to a chatbot, being transferred to a human, and then hearing those dreaded words: “How can I help you…

Read More Salesforce Clouds

Salesforce Clouds

Top 10 Salesforce Integration Services to Streamline Your Business in 2026

Disconnected systems represent one of the largest silent killers of business efficiency in 2026. Employees spend a significant portion of their workday switching between apps, manually re-entering data, or searching…

Read More Salesforce Services

Salesforce Services

Agentforce 360: Salesforce’s AI-Powered Service Console for the Agentic Enterprise

In the last few months, Agentforce 360 has been the gold standard for companies aiming to deliver on the vision of the agentic enterprise. Too often, support…

Read MoreReady to Make the Most Out of Your Salesforce Instance?

Our Salesforce aces would be happy to help you. Just drop us a line at contact@360degreecloud.com, and we’ll take it from there!

Subscribe to our newsletter

Stay ahead with expert insights, industry trends, and exclusive resources—delivered straight to your inbox.